Financials

Condensed Interim Consolidated Financial Statements For The Six Months And Full Year Ended 31 December 2025

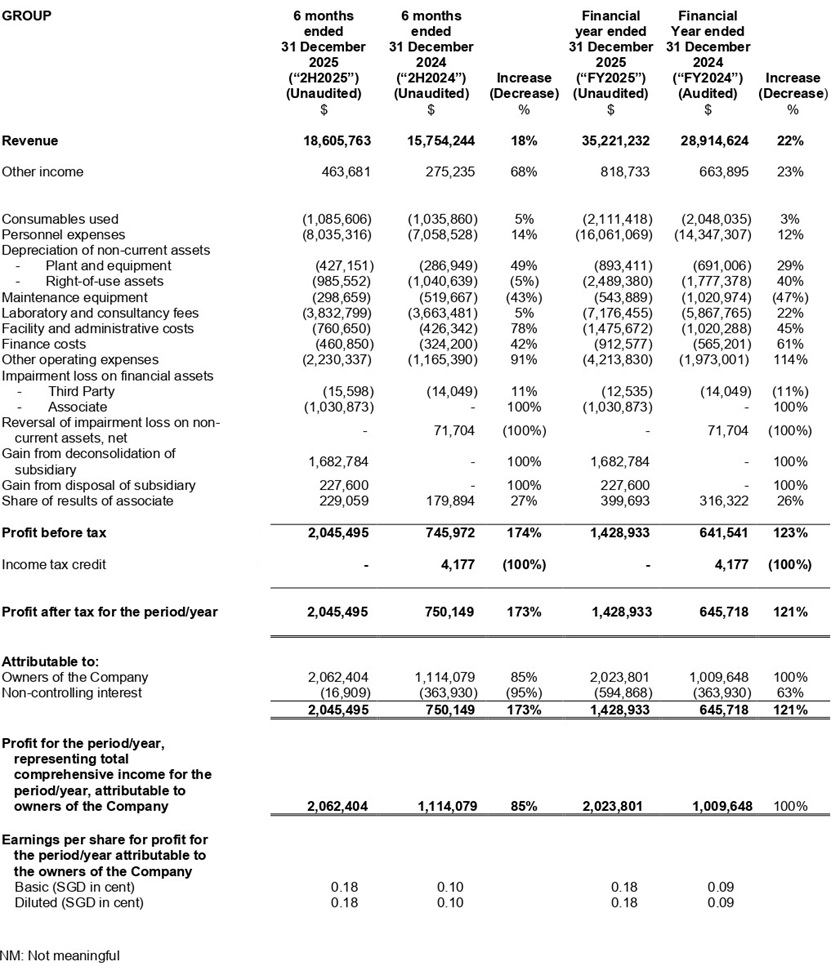

Financials ArchiveCondensed Interim Consolidated Statement Of Profit Or Loss And Other Comprehensive Income

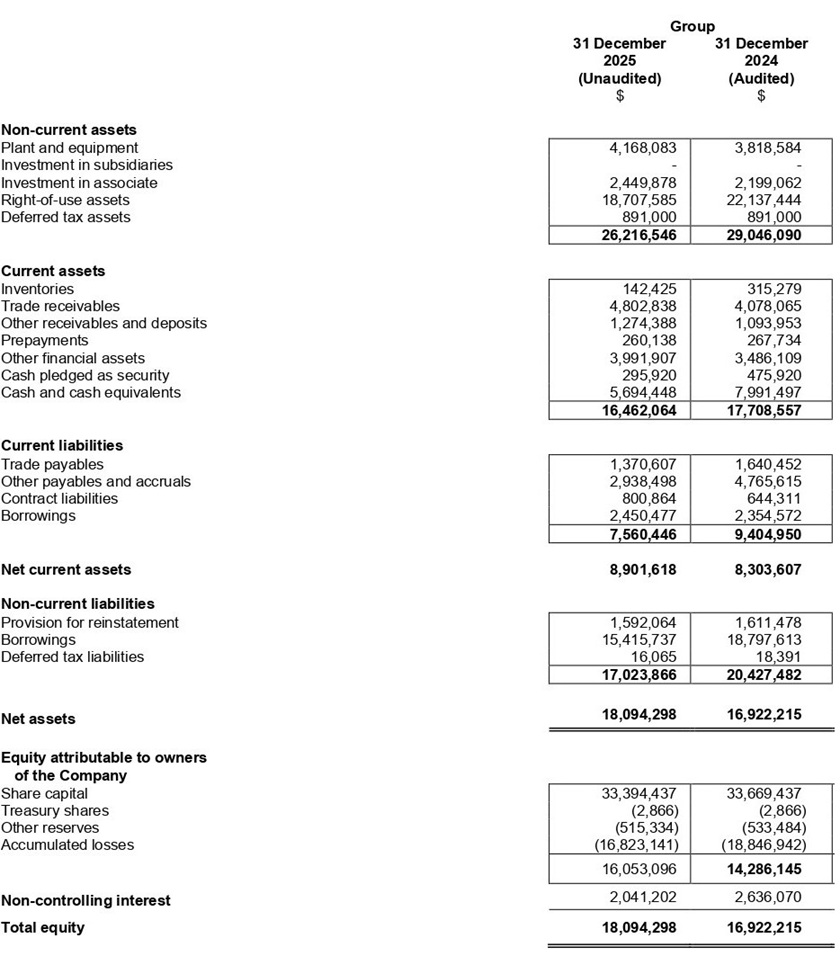

Condensed Interim Statements Of Financial Position

Review of Performance

2H2025 vs 2H2024

The Group recorded revenue of $18.6 million in 2H2025, representing an increase of $2.9 million (18%) compared to $15.8 million in 2H2024. The growth was primarily driven by higher contributions from diagnostic imaging services, which increased by $3.2 million (35%) from $9.2 million in 2H2024 to $12.4 million in 2H2025. The increase was supported by higher patient volumes and the continued ramp-up of the diagnostic imaging centre at Royal Square Medical Centre Novena. Diagnostic imaging remained the Group’s largest revenue contributor during the period.

The above increase was partly offset by lower contributions from medical aesthetic services following the disposal of the Group’s 60% equity interest in AATAC on 31 October 2025, as well as from primary healthcare services. Revenue from medical aesthetic services decreased by $0.4 million, or approximately 30%, from $1.2 million in 2H2024 to $0.9 million in 2H2025, as the Group deconsolidated AATAC upon completion of the disposal on 31 October 2025.

Other income increased by $0.2 million (68%) to $0.5 million in 2H2025, mainly attributable to a reversal of prior year’s interest accrual of $0.1 million and gain on disposal of plant and equipment of $0.1 million in 2H2025.

Operational costs increased broadly in line with business expansion. Personnel expenses increased by $1.0 million (14%) to $8.0 million, reflecting manpower additions to support increased imaging capacity and operations at Royal Square Medical Centre Novena. Laboratory and consultancy fees increased by $0.2 million (5%) to $3.8 million, largely in line with higher imaging volumes and collaboration with third-party service providers.

Facility and administrative costs rose by $0.3 million (78%) to $0.8 million, mainly due to higher administrative and service charges arising from business partnership arrangements with external healthcare providers, under which referral and collaboration activities increased during 2H2025 compared to 2H2024. Finance costs increased by $0.1 million (42%) to $0.5 million, primarily reflecting the full-year recognition of interest expenses on borrowings and lease liabilities, as the related financing arrangements had only commenced progressively during FY2024.

Depreciation of plant and equipment increased by $0.1 million (49%), reflecting additional capital expenditure on medical equipment. Depreciation of right-of-use assets slightly decreased by 5% due mainly to modification of right-of-use assets.

Maintenance equipment expenses decreased by $0.2 million (43%) to $0.3 million, primarily due to the reclassification of certain IT and software-related maintenance costs to other operating expenses compared with 2H2024. Correspondingly, other operating expenses increased by $1.1 million (91%) to $2.2 million, driven by full-year operations of the diagnostic imaging centre at Royal Square Medical Centre Novena in 2H2025.

The Group recognised the extraordinary net gain of $0.9 million during 2H2025 from the Group’s disposal of 60% interest in AATAC, completed in October 2025. Please refer to Note N9 and paragraph 21 of this announcement for further details.

Share of results from associate relates to Positron Tracers Pte Ltd (“PTPL”) and AATAC (upon completion of the Group’s disposal of 60% interest of AATAC in October 2025) which increased by 27% to $0.2 million, mainly resulting from improved performance of PTPL and contribution from AATAC in 2H2025.

As a result of the above, profit before tax increased significantly to $2.0 million in 2H2025 (2H2024: $0.7 million), representing an increase of 174%. Profit after tax rose correspondingly to $2.0 million, compared to $0.8 million in 2H2024.

Overall, 2H2025 reflects strong operational performance supported by higher revenue, cost discipline in selected areas, and the positive impact of the one-off extraordinary gains.

FY2025 vs FY2024

The Group recorded revenue of $35.2 million in FY2025, representing an increase of $6.3 million (22%) compared to $28.9 million in FY2024. The improvement was mainly driven by an increase of $7.2 million in revenue from the diagnostic imaging services, the Group’s largest revenue contributor, which grew significantly during the year supported by higher patient volumes, expanded operating capacity and contributions from the diagnostic imaging centre at Royal Square Medical Centre Novena. As a result, diagnostic imaging services accounted for a larger proportion of the Group’s overall revenue in FY2025.

Revenue from medical wellness and health screening services remained broadly stable at $9.6 million in FY2025, reflecting sustained demand for preventive healthcare services. Revenue from medical aesthetic services decreased by $0.8 million in FY2025, mainly due to the Group’s disposed of 60% equity interest in AATAC on 31 October 2025, following which the results of the business were consolidated only up to the date of disposal. Revenue from primary healthcare services remained relatively stable at $2.4 million in FY2025.

Overall, the Group’s revenue growth in FY2025 was primarily attributable to the continued expansion and strengthening of its imaging business, which remains the key driver of the Group’s operating performance.

Other income increased by $0.2 million (23%) to $0.8 million, primarily driven by a reversal of prior year’s interest accrual of $0.1 million and gain on disposal of plant and equipment of $0.1 million, partly offset by lower grant income in FY2025 as compared to FY2024.

Operating expenses increased in line with business expansion. Personnel expenses rose by $1.7 million (12%) to $16.1 million, reflecting workforce expansion to support higher service volumes and operations at the centre at Royal Square Medical Centre Novena. Laboratory and consultancy fees increased by $1.3 million (22%) to $7.2 million, largely in line with increased diagnostic imaging activities and collaboration with third-party service providers.

Depreciation of plant and equipment increased by 29%, reflecting additional capital expenditure on medical equipment. During the year, the Group reassessed the estimated useful life of certain medical equipment, resulting in a reduction in depreciation expense of approximately $0.4 million for FY2025 (see Note N2.2). Depreciation of right-of-use assets increased by 40% due to machines’ lease recognition and rental commitments associated with expanded facilities.

Maintenance equipment costs decreased by 47% to $0.5 million, mainly due to the reclassification of certain IT and software-related maintenance expenses to other operating expenses. Facility and administrative expenses increased by 45% to $1.5 million, in line with higher operating activities and expanded business operations during the year.

Finance costs increased by 61% to $0.9 million, primarily due to higher interest expenses on equipment financing and lease liabilities under SFRS(I) 16.

The Group recognised the extraordinary net gain of approximately $0.9 million during FY2025 from the Group’s disposal of 60% interest in AATAC completed in October 2025. Please refer to Note N9 and paragraph 21 of this announcement for further detail.

Share of results from associate increased by 26% to $0.4 million, reflecting improved performance of PTPL and contribution of AATAC as an associate subsequent to the deconsolidation of the business in October 2025.

Accordingly, profit after tax increased to approximately $1.43 million in FY2025 (FY2024: $0.65 million). Excluding one-off extraordinary gain, the improvement in profit was mainly attributable to higher revenue and operating leverage from increased service volumes. Profit for the year, including non-controlling interests, rose from $1.0 million in FY2024 to $2.0 million in FY2025.

Condensed Interim Statements of Financial Position

31 December 2025 vs 31 December 2024

Non-Current Assets

Non-current assets decreased by $2.8 million from $29.0 million as at 31 December 2024 to $26.2 million as at 31 December 2025. The decrease was mainly attributable to lower right-of-use assets, which declined to $18.7 million (FY2024: $22.1 million) following depreciation charges during the year. This was partially offset by an increase in investment in associate to $2.4 million (FY2024: $2.2 million), reflecting the Group’s share of profits recognised during the year, as well as additional plant and equipment acquisitions.

Current Assets and Current Liabilities

Current assets decreased by $1.2 million from $17.7 million as at 31 December 2024 to $16.5 million as at 31 December 2025, mainly due to a reduction in cash and cash equivalents to $5.7 million (FY2024: $8.0 million). During the year, the Group utilised cash to settle outstanding vendor balances, while surplus funds were also placed into short-term treasury instruments, including Treasury bills and non-callable bank deposits presented under other financial assets. Trade receivables increased in line with higher revenue and business activity during FY2025.

Correspondingly, current liabilities decreased by $1.8 million from $9.4 million to $7.6 million, driven by lower trade payables and other payables and accruals following payments made to suppliers and service providers during the year. Contract liabilities and short-term borrowings increased marginally in the normal course of operations.

These movements reflect higher operating activity during the year, with increased receivables arising from revenue growth alongside the settlement of prior-period obligations.

Net Current Assets

Net current assets increased to $8.9 million as at 31 December 2025 compared to $8.3 million in FY2024, reflecting the settlement of outstanding payables during the year alongside higher trade receivables arising from increased revenue.

Non-Current Liabilities

Non-current liabilities decreased from $20.4 million as at 31 December 2024 to $17.0 million as at 31 December 2025, mainly due to a reduction in borrowings following higher loan repayments during the year. The increased repayments were in line with the commencement of operations at Royal Square Medical Centre Novena, for which financing had previously been obtained. Provisions for reinstatement obligations and deferred tax liabilities remained relatively stable.

Non-controlling interest

Non-controlling interests decreased from $2.6 million to $2.0 million as at 31 December 2025, mainly reflecting the share of results attributable to non-controlling shareholders during the year.

Condensed Interim Consolidated Statement of Cash Flows

Net cash generated from operating activities increased to $3.9 million in FY2025 (FY2024: $2.5 million), reflecting improved operating performance and cash generation from core operations. Net cash used in investing activities amounted to $3.0 million, mainly relating to capital expenditure on plant and medical equipment and placements into short-term Treasury bills as part of treasury management.

Net cash used in financing activities of $3.2 million was primarily attributable to scheduled repayment of borrowings and interest payments following the commencement of operations at Royal Square Medical Centre Novena. Consequently, cash and cash equivalents stood at $5.7 million as at 31 December 2025 (FY2024: $8.0 million), reflecting the Group’s deployment of cash towards operational expansion and debt servicing while continuing to generate positive operating cash flows.

Commentary

The healthcare and diagnostic imaging industry in Singapore continues to benefit from favourable long-term fundamentals driven by an ageing population, growing healthcare awareness, and increasing demand for preventive healthcare and diagnostic services. However, the operating environment remains competitive, with ongoing challenges relating to manpower shortages, rising labour costs and increasing operating expenses across the healthcare sector.

During FY2025, the Group expanded its diagnostic imaging capacity with the commencement of operations at Royal Square Medical Centre Novena, which complements the Group’s existing integrated medical centre at Orchard Road. The additional capacity positions the Group to meet growing demand from specialist clinics, hospitals and corporate healthcare providers, while strengthening its presence in key medical hubs in Singapore.

Following the operational ramp-up of our operations at Royal Square Medical Centre Novena, the Group expects to focus on improving operational efficiency, optimising utilisation rates and enhancing service delivery to support sustainable performance over the next 12 months. Continued investment in technology, workflow optimisation and talent development remains necessary amid competition for skilled healthcare professionals.

Industry trends towards preventive healthcare, employee wellness programmes and national health promotion initiatives are expected to continue supporting demand for the Group’s health screening and wellness services. Government-led healthcare initiatives and increasing emphasis on early detection are anticipated to contribute positively to service volumes in the coming periods.

The Group expects lower contribution from its On-site healthcare services segment in the next reporting period following the conclusion of the Health Promotion Board (“HPB”) school health screening project, for which the Company was not awarded the subsequent tender announced in late 2025. While the project contributed positively in prior periods, management continues to explore alternative on-site healthcare opportunities and corporate screening engagements to support segment performance.

Looking ahead, the Group will continue to strengthen strategic partnerships and explore opportunities to expand integrated healthcare services while maintaining prudent cost management and operational discipline. While cost pressures and competitive dynamics are expected to persist, management remains cautiously optimistic about the Group’s prospects for the next reporting period and the next 12 months.